What's happening with interest rates?

Will they drop even lower or is the lowering cycle running out of steam? And what do low interest rates mean for investors?

When the Reserve Bank of Australia (RBA) lowered the official interest rate (cash rate) to 3.25% at the depths of the global financial crisis in February 2009, we entered new economic territory. Never before had the cash rate fallen below 4% in Australia.

Since that time, we have grown accustomed to interest rates below 5%. Some commentators even believe we may even see rates go below their current record low of 2.5%.

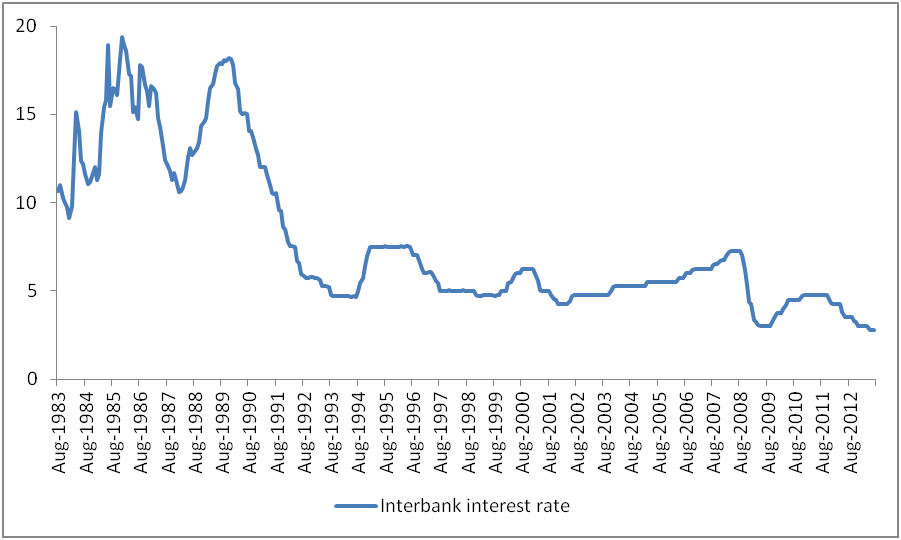

Chart 1. Australian interest rates 1983 - 2013

Source: Reserve Bank of Australia

As you can see from Chart 1, this period of very low rates is unusual from a historical perspective. Before 2009, the last time interest rates went below 5% was in September 2001 when the economic downturn that followed the bursting of the internet-fuelled sharemarket bubble was further compounded by the September 11 terrorist attacks in New York.

Interest rates have risen as high as 19.4% - during the period of high inflation in the mid-1980s. In an attempt to combat the inflationary pressures, the RBA kept rates above 15% for two years from April 1985 and a further 18 months from February 1989.

BT Chief Economist Chris Caton says the reason rates are now so low is that the outlook for inflation is benign and the Australian economy is showing signs of weakness as the mining boom fades.

“At the moment, it is hard to be optimistic about the Australian economy with the prospect of subdued growth and rising unemployment,” he says.

“The low inflation outlook gives the RBA more flexibility to reduce rates in an effort to stimulate economic activity.”

Effect on investors

Low interest rates are unequivocally good news for people with mortgages. For investors relying on cash and term deposits for income, it is generally bad news. According to the RBA, the average one year term deposit rate has fallen from above 6% just before the latest round of official interest rate cuts began in 2011 to around 3.7% in July 20131.

For fixed interest investors, low interest rates in themselves are not bad. What is more important is the direction of interest rates. Periods of falling interest rates tend to bolster fixed interest returns while periods of rising rates tend to restrain returns.

When official interest rates are falling, the capital value of bonds tends to increase as investors are willing to pay more for bonds offering higher rates on interest than new bonds being issued. For example, let’s say you bought a 10-year bond yesterday paying an interest rate of 5%. If interest rates halved overnight to 2.5%, then the income from the interest payments from the bond would be twice as valuable. The opposite occurs when official interest rates rise.

Growth assets such as shares and property have an even more complex relationship with interest rates. Growth assets do not respond mechanically to changes in interest rates as they are influenced by many other factors such as changes in expectations and general business cycle conditions, Mr Caton says.

“All other things equal, falling interest rates tend to be good news for share and property investors,” he says.

Lower interest rates reduce the cost of borrowing for households, investors and businesses. This may translate into improvements in household balance sheets, consumer spending and business profits. It also makes borrowing to invest more attractive for investors and businesses.

“However, falling interest rates are often a response to a negative economic growth outlook which is generally bad news for shares and property,” Mr Caton says.

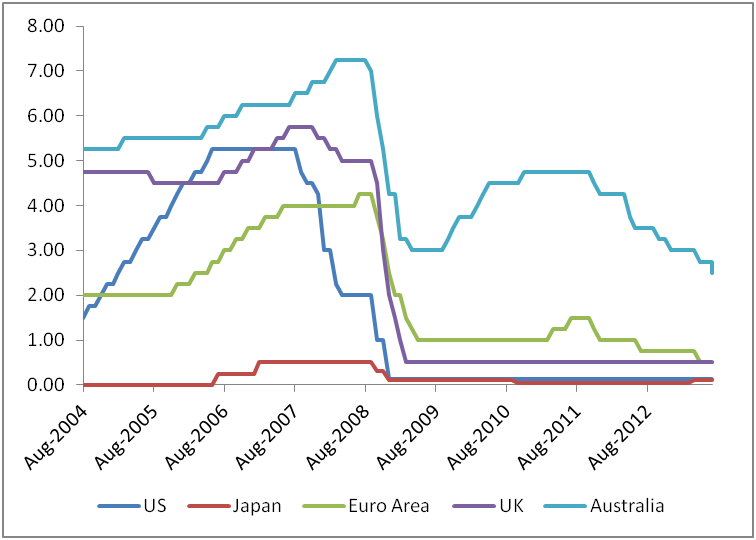

Interest rates can also have a significant effect on returns from international shares, property and bonds, due to their effect on our currency. Our dollar tends to be stronger when our interest rates are higher than those of other major economies, which in turn will reduce returns from unhedged international investments, such as those held by many super funds. The opposite is true when the gap between our interest rate and those of other major economies shrinks, as it did in May and June this year, as you can see from Chart 2.

Chart 2. Australian interest rates compared to leading economies 2004-2014

Source: Reserve Bank of Australia

Outlook

Like all investment markets, predicting short-term movements in interest rates is very difficult. Some economists believe the RBA may cut rates a further 0.5% in the coming year. They point to downbeat comments on the short-term prospects for the Australian economy by the RBA and the absence of any indicators of pressures on inflation.

Mr Caton says he believes the interest rate cycle is close to its low point.

“The market has priced in one or two rate cuts over the next 12 months,” he says.

“However, with the current rate at 2.5%, the RBA is running out of ammunition to stimulate the economy. It has also indicated it is prepared to wait to see the effects of the recent cuts.”

Mr Caton also points out that the cycle can turn faster that many expect.

“What surprises many people is how quickly the RBA has moved in the past from reducing rates to raising them again, such as in 2001 and 2009,” he says.

“In the past, only around six months has separated the last rate cut and first rate rise.”